There’s been so much news on the coal export front of late — the massive scope of the proposed Gateway-Pacific terminal’s Environmental Impact Statement; the Lummi Nation’s unequivocal opposition to a coal terminal at Cherry Point; and recent revelations about the ongoing financial woes of coal terminal developer Ambre Energy — that it’s hard not to sense that Northwest coal export projects are on the ropes.

But perhaps the most important coal export story has gotten surprisingly little attention — the collapse of Pacific Rim coal prices. With the latest price decline, I think we can definitively call the hype over Northwest coal export projects for what it always was: a bubble.

But to see why the inflated hopes for Northwest coal exports were the product of a bubble mentality, you have to look at the long-term price trends.

Click to embiggen.

Starting in early 2009, Pacific Rim coal prices began a rapid, 22-month rise — lifted, in part, by surging demand from China for imported coal. And as prices soared, would-be U.S. coal exporters saw a business opportunity, hatching plans for six different coal export terminals in Washington and Oregon to service the Pacific Rim coal market.

But their timing was terrible. The surge in international coal prices wasn’t permanent. In retrospect, it showed all of the classic signs of a bubble.

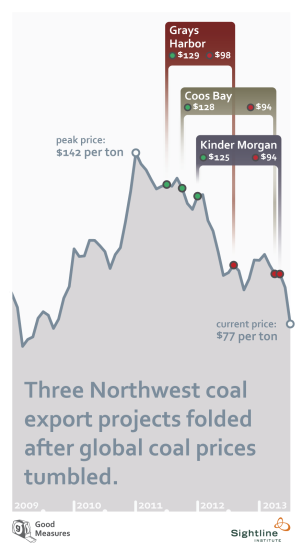

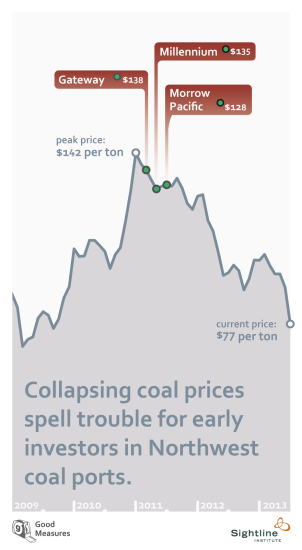

As it turned out, each of the six proposed export projects was launched after Pacific Rim coal prices had already peaked. Prices dipped from their January 2011 high, and stabilized in the $120-$130 range for nearly a year. But only a year after they peaked, Australian benchmark coal prices plummeted, quickly falling below $100.

At that point, and with no sign of a price recovery on the horizon, three of the coal terminal proponents gave up the ghost.

The fall in coal prices was somewhat predictable. As coal prices skyrocketed, established exporters such as Indonesia and Australia boosted output, and China took steps to make its own coal industry more efficient. Meanwhile, growth in Chinese electricity demand slowed. That combination — slower demand growth, massive supply increases — pulled coal prices back to earth.

Click to embiggen.

Coal prices have sunk even lower since the last of those three terminal proposals folded. For the last month, Australian benchmark coal prices have hovered around $77 per ton, or $65 per ton below their 2011 peak. That means that prices have fallen back to where they were in the middle of 2009 — back when massive U.S. coal exports were just a pipe dream. At this point, the early investors in the three remaining Northwest coal terminal projects must be sweating bullets.

Global minerals analysts have been sounding the alarm about coal prices for months. Back in February, IHS-CERA published a report forecasting a near-term peak in Chinese coal imports, followed by a long-term decline, and warned that China’s coal market was not the “Promised Land” that coal companies were hoping for. Researchers for Greenpeace International reached the same conclusion. Then in May, Deutsche Bank predicted that coal markets would remain oversupplied for a decade. And then just last week, Goldman Sachs announced that due to global oversupply of coal, “The window for thermal coal investment is closing.” (David Roberts has a nice writeup.) At this point, the most bullish, pro-coal analysts believe that

exports could reasonably hit 30 million tons of coal from the Northwest, or about a third of the capacity currently proposed to move through the export facilities still being proposed.

That’s right, the “bulls” are now saying that two-thirds of the Northwest’s coal export capacity will simply sit idle.

So as you read about the legal, regulatory, and financial hurdles that coal terminal developers face, remember the economic backstory: Northwest coal terminal developers launched their projects just as the Pacific Rim coal bubble was starting to deflate. Coal terminal proponents are now facing their toughest tests — regulatory hurdles, community opposition, and cash crunches — in a backdrop of a precipitous price decline and increasingly desperate economic fundamentals.