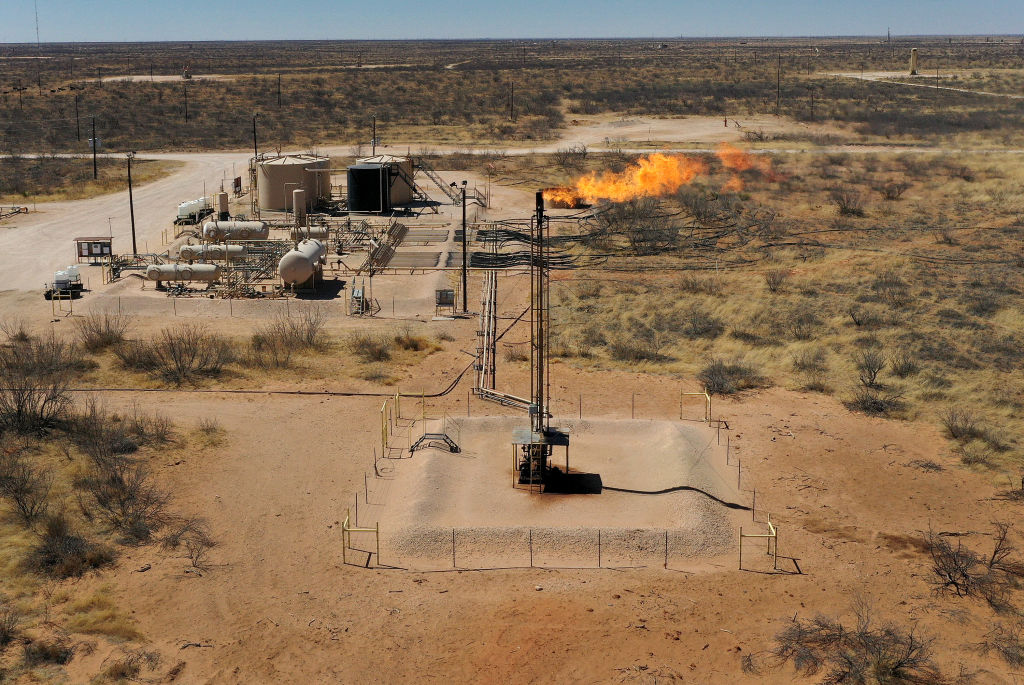

The Inflation Reduction Act, the 2021 U.S. climate law abbreviated IRA, primarily reduces emissions through financial incentives, rather than binding rules. But in addition to all its well-known carrots, lawmakers quietly included a smaller number of sticks — particularly when it comes to the potent greenhouse gas methane, which has proven to be a pesky source of increasing climate pollution with each passing year. New research suggests that those sticks could soon batter the oil and gas industry, which is responsible for a third of all methane emissions in the U.S.

An IRA provision directs the Environmental Protection Agency, or EPA, to charge $900 for every metric ton of methane above a certain threshold released into the atmosphere in 2024. The issue is particularly challenging to tackle in oil and gas fields because methane is the primary component in natural gas, and it leaks from hundreds of thousands of devices scattered across the country. In 2022, oil and gas facilities emitted more than 2.5 million metric tons of methane.

The methane fee is one of a handful of ways in which the Biden administration is trying to get the industry to clean up its act. Late last year, the EPA finalized a rule requiring drillers to take comprehensive measures to monitor for and fix methane leaks. Separately, the agency is revising a rule that governs how companies count up and report the volume of methane emissions from their operations. That rule in particular will determine the EPA’s ability to assess the success of its methane reduction rule and help it calculate defensible fees to penalize companies for their emissions.

A new analysis by Geofinancial Analytics, a private data provider, found that some companies may be liable for tens of millions of dollars in fees — a possibility that could bankrupt some operators. The analysis, which relied on satellite data, found that the top 25 oil and gas producers in the country would together have been liable for as much as $1.1 billion if the methane fee was applied to emissions for a one-year period ending in March 2023.

On the one hand, major players like Chevron and Shell, which have publicly welcomed the new methane fee rule, are well below the rule’s threshold for penalizing emissions, according to Geofinancial. (This is likely due to large companies’ relative technological sophistication and economies of scale.) The fee only goes into effect when companies emit methane at volumes equivalent to more than 25,000 tons of carbon dioxide, which means that smaller companies, too, are largely exempt from the rule. Still, a 2022 congressional analysis found that, despite the exemptions, the rule should effectively penalize about a third of all methane emissions from U.S. oil and gas infrastructure.

As a result, industry trade groups like the American Petroleum Institute, which represents a large swath of the oil and gas industry, have pilloried the rule and backed a proposal to repeal the fee.

Some of the largest potential liabilities stemming from the rule, according to Geofinancial’s analysis, belong to Diversified Energy Company, a seasoned operator with about two decades in the oil and gas industry but an unusual business model. While the Exxons and Chevrons of the world typically rely on drilling new wells and increasing fossil fuel production to generate revenue, Diversified’s growth is heavily dependent on buying old wells at the end of their lives and wringing every last bit of oil or gas out of them. These low-producing wells come with serious environmental liabilities: The older the well, the more expensive it is to complete the required steps to seal it and prevent additional pollution — and the more likely it is to leak copious amounts of methane.

Diversified, which has become the largest owner of oil and gas wells in the U.S., has some 70,000 such old and potentially leaky wells — making it potentially one of the biggest methane emitters in the industry as well. According to Geofinancial, Diversified would be liable for as much as $184 million if its annual excess methane emissions are equivalent to what it released over the year ending in September 2023. While the satellite results are a snapshot in time and contain some uncertainty, Geofinancial’s overall finding is that Diversified is probably facing catastrophically steep methane fees — an outcome that Diversified disputes, arguing that it has lowered its methane intensity such that it will be exempt from the new fees.

This potential liability is one of the reasons twin brothers Henry and Chris Kinnersley, founders of the activist investing firm Snowcap Research, are betting Diversified will fail. The brothers are shorting Diversified’s stock — making a big bet, essentially, that the company’s stock value will fall.

“To put the methane fee in context, in the last 12 months Diversified’s free cash flow was $172 million,” said Chris Kinnersley. “We estimate nearly all of this was required to fund new acquisitions to offset the company’s declining production.”

John Sutter, a spokesperson for Diversified, said that the company has taken proactive measures to crack down on methane and that the practices are resulting in significant emissions reductions. “Diversified’s stewardship model shows a viable path forward for mature well operators: that it is possible to cut methane emissions and responsibly manage existing producing assets,” he said.

Part of the reason for the diverging expectations could be that quantifying methane emissions is fundamentally a difficult undertaking. The industry is required to submit its own estimates to the EPA’s greenhouse gas reporting program, but those numbers are widely understood to be an undercount. One study by the nonprofit Environmental Defense Fund found that the industry’s figures may be 60 percent lower than actual emissions. (Editor’s note: The Environmental Defense Fund is an advertiser with Grist. Advertisers have no role in Grist’s editorial decisions.)

Based on research largely from the 1990s, the EPA has developed emission factors for every type of equipment found in oil fields. That means that, to comply with the EPA’s rules, operators first count up the various methane-emitting devices they own and operate, then multiply the number of devices by the corresponding emission factor to arrive at their total emissions for the year.

This approach falls short for two major reasons. When devices fail or malfunction, they tend to release large volumes of methane well above those accounted for by the emission factor — but the industry currently isn’t required to report these large releases. Additionally, the EPA’s emission factors are outdated, having been developed decades ago, well before the fracking revolution. New drilling and production technology has led to new and increased sources of methane releases, which the agency’s emission factors don’t fully capture.

Since calculating a fee to levy on operators requires an accurate and defensible count of the methane companies are spewing, the EPA proposed updating the reporting requirements last year. The proposed rule contains updated emissions factors based on new research. It also requires companies to report large releases if they become aware of them. Still, these measures aren’t expected to fully eliminate the gap between the emissions companies are reporting on paper and true emissions.

“It’s likely to help close the gap but not get all the way there,” said Edwin LaMair, an attorney at the Environmental Defense Fund. “A lot of those large releases will not be seen and then won’t be reported.”

To increase the probability that large releases are caught, the EPA’s regulations include a provision for watchdog groups to report methane data independently. Over the last few years, the capabilities of satellite technology and aerial flights have been leveraged to get more accurate information about methane emissions from oil and gas fields. Nonprofit groups like the Environmental Defense Fund, for instance, have conducted aerial flights over the Permian Basin, the largest oil-producing region in the U.S. Earthworks, another environmental group, has long used infrared cameras to observe well sites and report faulty equipment. That empirical evidence can now be independently submitted to the EPA for consideration as it calculates methane fees for companies.

In particular, satellite data is expected to play an important role in holding companies accountable. The Environmental Defense Fund, for instance, is planning to launch its own satellite in the coming months to monitor methane. The data from the satellite is expected to be posted to a public website.

There’s also the data from existing satellites, which firms like Geofinancial have utilized. The data provider relied on a satellite launched by the European Space Agency that can provide a resolution of one square kilometer at best. In dense oil fields like the Permian in Texas and the Bakken in North Dakota, there are often multiple wells owned by different companies within a square kilometer. Scientists at Geofinancial used statistical methods to attribute emissions to specific operators, but there is some inherent uncertainty in the estimates. While the findings may not be precise, they are still valuable to investors and the public trying to grasp a company’s contribution to the methane problem and its potential financial liability.

“We’re conveying the empirical data, which has plus or minus error bars on it,” said Mark Kriss, the managing director at Geofinancial. “Even at a given wellhead, a one-kilometer pixel, in many cases, we have pretty good confidence about who’s responsible for that, but not in every case. But when you aggregate things at the company level, we have very high confidence.”

For investors like the Kinnersleys, that data is valuable even with all its uncertainty. Until 2021, Diversified calculated its methane emissions using the EPA’s methodology. But that year, the company switched to a method developed by the Intergovernmental Panel on Climate Change, which allows companies to self-measure emissions in the field. The company claimed that the measurement-based work “highlighted the negative implications of using prescribed, theoretical emissions factors in our calculations as compared to using the actual measurements from the true operations of our assets.”

The resulting emissions were 60 percent lower than in previous years — and, as a result, lowered the firm’s methane-intensity close to a threshold that would exempt it from the new U.S. government fee. The main difference came from how the company estimated its emissions from pneumatic devices, which are used to move fluids. The EPA’s method requires that the company use an emission factor of 13.5 for pneumatic devices, but the company calculated a lower emission factor of 5.5 through measurements in the field.

“As a third party, it’s very difficult to verify whether that new, updated emission factor is actually fair,” countered Chris Kinnersley. “There’s lots of ways you can game that. You can go to newer wells at certain times and you can say, ‘Hey, we sat outside this well, and it was only emitting this much.’”

Sutter, the Diversified spokesperson, did not respond directly to questions about the Kinnersleys’ allegations, but the company told Bloomberg that the brothers’ “report contains numerous inaccuracies, ignores specific financial and operational results and sustainability actions, and is designed for the sole purpose of negatively impacting the company’s share price for the short seller’s own benefit.”

As satellite technology matures and the EPA’s rules for reporting are finalized, advocates expect transparency around methane emissions will increase. The EPA is expected to audit the emission numbers that companies turn in more closely.

“They’re going to be beefing that process up in light of the methane fee, since now there’s a financial incentive to misreport their emissions or omit certain things,” said LaMair. “They’ll be able to find these discrepancies, continue to improve their reporting methodologies, and find the companies that might be underreporting.”

This story has been updated to incorporate comments received from a Diversified Energy spokesperson after publication.

A message from

Your support keeps our climate news free.

Grist is the only award-winning newsroom focused on exploring equitable solutions to climate change. It’s vital reporting made entirely possible by loyal readers like you.

At Grist, we don’t believe in paywalls. Instead, we rely on our readers to pitch in what they can so that we can continue bringing you our solution-based climate news. Donate today to keep our site free.