I like to think of myself as a reasonably cynical person, at least in matters of finance.

When I started reporting on Mexico’s markets in 1998, Russia had just defaulted in billions of debt. Russia and Mexico had virtually no direct financial or trade relationship, yet large investors punished Mexico anyway. (To be fair, Mexico still hadn’t recovered from its own financial meltdown of a few years before.) The peso plunged against the dollar, sparking something close to hyper inflation. I watched in awe as working people’s real wages — my own included, since I was paid in pesos — dropped by about 5 percent per month.

I moved to New York City in 1999, as the dot-com bubble entered what turned out to be its final puff-up. As a senior editor at a Wall Street trade magazine, my desk commanded a magisterial view of New York Harbor from 15 gleaming stories in the air. Within two years, the Nasdaq had surrendered something like 80 percent of its value. My next office was in the windowless bowels of a seedy Lower Manhattan building.

I haven’t seen it all, but I’ve seen plenty. Nothing has prepared me for the federal government’s $85 billion takeover of what’s left of the world’s biggest insurance company. Let’s look at the details of this unprecedented deal.

When the stock market closed Tuesday, investors were valuing AIG at $10 billion — and threatening to take it lower. The Federal Reserve swooped in with $85 billion in public cash — in return for 80 percent of AIG shares.

Let’s see: 80 percent of $10 billion is $8 billion. So for our $85 billion layout, we — i.e, the taxpayers — got $8 billion in value. We overpaid for AIG by a factor of more than ten.

And what do we get for our investment? AIG isn’t just an insurance company — it’s a sprawling financial giant, and a poster child for the deregulatory fever that has governed U.S. financial markets since the 1990s.

For decades, the Depression-era Glass-Steagall Act kept insurance underwriters, stock underwriters, and traditional lenders separate. Then in the 1990s, as this excellent Frontline report shows, Congressional Republicans worked with the Clinton Treasury to undermine Glass-Steagall. The venerable act finally toppled in 1999.

Depressing presidential campaign note: two of the chief instigators of Glass-Steagall’s demise — Robert Rubin and Phil Gramm — are now top economic advisers to Obama and McCain, respectively.

With annoying Glass-Steagall taken care of, former AIG chief Hank Greenberg — not so long ago the most formidable player on Wall Street — began taking cash generated by the ever-profitable but boring insurance business and building out a financial-services empire.

Soon enough, AIG began making billions insuring newfangled Wall Street products like those now-infamous mortgage bundles and "collatoralized debt obligations."

Everything was more or less rosy (though Hank Greenberg did resign in disgrace over an accounting scandal) until 2007, when Wall Street’s mortgage-back house of cards collapsed.

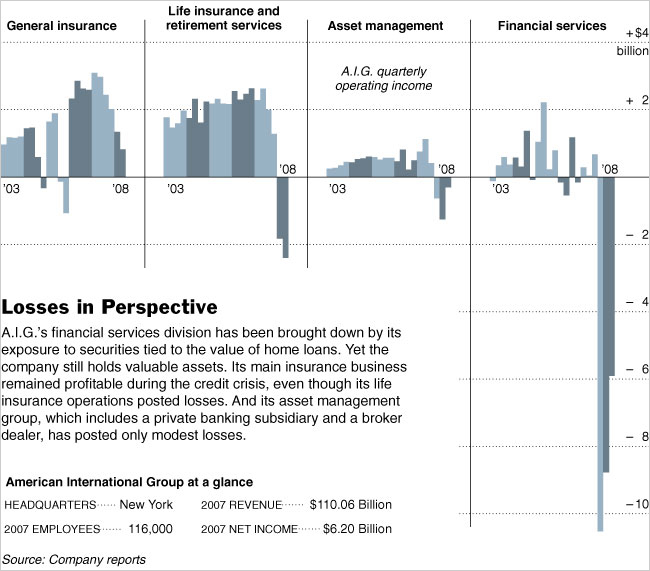

So, again, what are we getting 80 percent of today, for our $85 billion? Check out this New York Times graphic. We get a moderately profitable (but declining) traditional insurance company, alongside a financial services firm that has hemorrhaged $27 billion in the last three quarters alone.

And who’s on the line for the company’s massive expected future losses? We are.

Some will argue that we’re getting much more than a wrecked company for our investment. In this view, the Fed had to step in to bail out AIG, because if the insurance giant had failed, financial chaos would have gained steam. That’s no doubt true.

But guess what? Financial chaos is gaining steam anyway. As I write this, shares in the two remaining Wall Street investment banks — Goldman Sachs and Morgan Stanley — are cratering. Within days, failing some miracle, they’re likely either be bailed out at our expense, or folded into large traditional banks, where federally insured deposits can be raided to offset their losses. In other words, either way, untold billions more out of the Treasury.

And get this: In the wake of the AIG buyout, Standard & Poor’s is now considering slashing the U.S. government’s credit rating. That move would significantly jack up the federal government’s cost of borrowing money — which it will be doing plenty of, given this ongoing mess and the other ones in Iraq and Afghanistan.

As I wrote two days ago, we’re entering the era of climate change with a severely overextended Treasury — a dwindling financial position from which to invest in public-transportation infrastructure, low-carbon energy sources, etc. And that statement is even more painfully true today.

What’s gotten us here is a now-discredited, quasi-religious fantasy that unregulated markets dominated by a few big players lead to ever-increasing prosperity. What we really get is a system that privatizes profit — any chance that execs from Bear Stearns, Lehman, Fannie Mae, Freddie Mac, or AIG will pony up any savings from their kingly recent salaries? — and socializes risk.

What we really get is a federal government that can’t get it together to tackle urgent social or ecological problems — but that can mobilize billions in a flash to bail out banks.

As the eminent economist Joseph Stiglitz recently wrote:

We had become accustomed to … hypocrisy. The banks reject any suggestion they should face regulation, rebuff any move towards anti-trust measures — yet when trouble strikes, all of a sudden they demand state intervention: they must be bailed out; they are too big, too important to be allowed to fail …

The present financial crisis springs from a catastrophic collapse in confidence. The banks were laying huge bets with each other over loans and assets. Complex transactions were designed to move risk and disguise the sliding value of assets. In this game there are winners and losers. And it’s not a zero-sum game, it’s a negative-sum game: as people wake up to the smoke and mirrors in the financial system, as people grow averse to risk, losses occur; the market as a whole plummets and everyone loses.

A message from

Your support keeps our climate news free.

Grist is the only award-winning newsroom focused on exploring equitable solutions to climate change. It’s vital reporting made entirely possible by loyal readers like you.

At Grist, we don’t believe in paywalls. Instead, we rely on our readers to pitch in what they can so that we can continue bringing you our solution-based climate news. Donate today to keep our site free.

{kind=link}