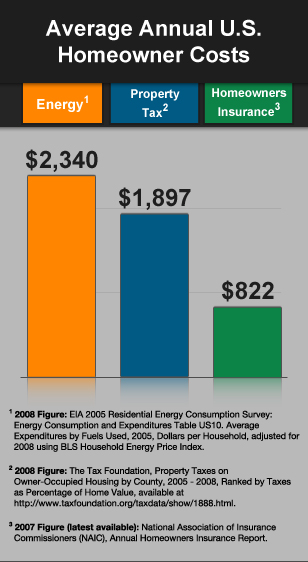

Via Institute for Market TransformationLet’s talk home economics: The average American household spends $2,340 to heat, cool, and electrify its home for a year, according to the Department of Energy.

Via Institute for Market TransformationLet’s talk home economics: The average American household spends $2,340 to heat, cool, and electrify its home for a year, according to the Department of Energy.

That’s more than average annual spending on property taxes ($1,900) and homeowner’s insurance ($800). Over the course of a 30-year mortgage, energy costs amount to $70,000 — a big chunk of change, especially when you consider that the median home price in the U.S. is $177,000.

Actual costs will vary, of course, depending on regional climate, the size and efficiency of the home, and how many sweaters you’re willing to wear in the winter. Homeowners can save as much as $400 a year if their homes are built to the International Energy Conservation Code [PDF], and more if they go beyond that standard.

Smart homebuyers (and renters) will factor energy costs into decisions about where to live. You’d think mortgage lenders would consider energy costs too — they need to know whether potential buyers can afford a particular home. But lenders largely ignore energy expenses, since they’re not a part of standard mortgage underwriting criteria.

That would change under the SAVE (Sensible Accounting to Value Energy) Act [PDF], a bill backed by Sen. Michael Bennet (D-Colo.) that would require lenders to consider energy costs before granting a borrower a federally insured mortgage. Bennet is considering introducing the bill after the August congressional recess, his office said, and it could end up as part of a larger banking or energy bill.

Residential buildings account for 21 percent of the nation’s energy use, so cleaning up the housing supply is a major climate imperative.

“Energy-efficient mortgages” have been available for years, running on the premise that borrowers who spend less on utility bills have more money available for mortgage payments. But they’ve been an underused niche product that few buyers or even lenders know about. The SAVE Act would take the concept and apply it to all government-sponsored mortgage enterprises, such as Fannie Mae, Freddie Mac, and the Federal Housing Administration. Those three entities currently guarantee more than 90 percent of new loans, so the bill would have a profound effect on ramping up home efficiency.

“The big news is that this would become a part of every federally backed mortgage,” said Cliff Majersik of the Institute for Market Transformation, an efficiency advocacy group that helped draft the bill.

For lenders, the bill removes a significant blind spot, according to Majersik. “By ignoring those energy costs, they’re ignoring an important factor in affordability,” he said. “By calculating energy costs, they’re doing better, more accurate underwriting. They’ll do a better job of not lending people more money than they can afford, and, conversely, they’ll do a better job of not rejecting people who are well-qualified to borrow, in part because they have lower energy costs.”

Energy costs would be measured in one of two ways — through a third-party report if available, or through estimates, based on home size, from the Energy Department’s Residential Energy Consumption Survey.

The change would encourage home buyers to demand more efficient homes, reforming a current system that essentially penalizes efficiency. Under current standards, a buyer may understand that a $6,000 up-front investment in high-efficiency windows, lighting, and a furnace will more than pay for itself over time, but that doesn’t mean a bank is willing to lend the buyer $6,000 more. And a home builder might also be hesitant to add that $6,000 worth of improvements, since they would only make it harder for buyers to qualify for financing. The SAVE Act would remove that disincentive.

The change would encourage home buyers to demand more efficient homes, reforming a current system that essentially penalizes efficiency. Under current standards, a buyer may understand that a $6,000 up-front investment in high-efficiency windows, lighting, and a furnace will more than pay for itself over time, but that doesn’t mean a bank is willing to lend the buyer $6,000 more. And a home builder might also be hesitant to add that $6,000 worth of improvements, since they would only make it harder for buyers to qualify for financing. The SAVE Act would remove that disincentive.

The bill has the support of the Leading Builders of America, a trade group that represents 16 of the largest construction companies in the nation.

“The big barrier with energy efficiency has always been how to pay for it,” said LBA Policy Director Clayton Traylor. “Customers love it, but they either don’t want to pay for it or can’t pay for it under existing mortgage guidelines.”

He said home energy standards (such as Energy Star) are an increasingly important part of marketing new homes, but that, without lending reforms, efficiency must compete with other amenities — like hardwood floors and stainless-steel appliances — for priority in a buyer’s budget.

The bill does not have support from the National Association of Homebuilders, a much larger trade group that has opposed energy-efficient mortgages in the past. It may face resistance from real-estate groups as well, since some energy-sucking homes might fare worse on the market when energy use is made visible.

The Obama administration could enact many of the the SAVE Act’s elements on its own, Majersik said, as it examines federal housing policy and considers plans to offload Fannie and Freddie. But he and other key architects of the bill would prefer comprehensive legislation.

Even if Bennet introduces the SAVE Act this year, it many not go anywhere soon. As with anything in the Senate, inaction is always more likely than action — even though the bill is designed to have no budget or deficit impact.

“We don’t have any illusions that this is anything but an uphill climb in Congress,” said Traylor. “We’re committing to pushing this next year.”

Read about another tool that could green housing policy: location-efficient mortgages.